The length of time Does brand new FHA Loan Preapproval Techniques Get?

step 1. Come across a lender

Of numerous finance companies, borrowing unions, and online lenders render FHA financing. You can make use of a large financial company otherwise do some searching online examine FHA lenders’ ideal readily available rates of interest. You can examine all the-inside the FHA home loan can cost you ranging from no less than three mortgage brokers so you’re able to find a very good terms for the state. Without a doubt, your regional bank or credit connection is an FHA bank currently, in order to also examine the rates.

Opting for a reliable and you will educated financial that will help you regarding the financial processes is essential. You can check lender ratings towards Bbb and you may with other on the web comment internet. You could consider an excellent lender’s many years in business and you can whether or not this has gotten people problems about Individual Monetary Security Agency.

dos. Assemble Called for Papers

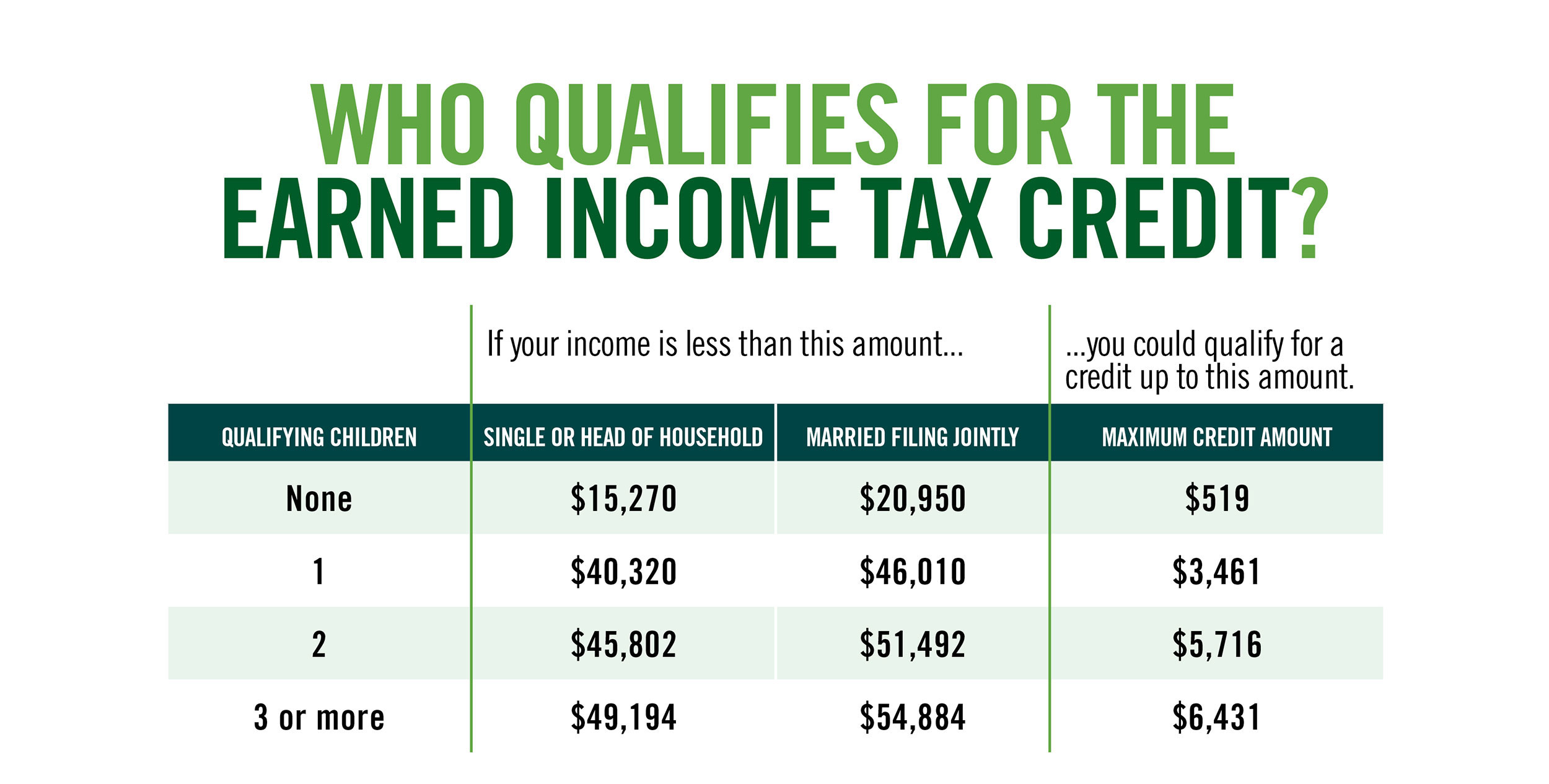

- Government-provided ID instance a driver’s license otherwise passport

- Your own Personal Security card and/or Societal Safety matter

- For the past a few months’ spend stubs

- Taxation statements and you can W-2s for the past 2 years

- Costs otherwise debts that show up on your credit history

- Lender statements that show offers to possess an advance payment.

- Confirmation of employment

3. Submit The loan Software

You have the solution to submit applications on the web or perhaps in person. Its important to fill in most of the suggestions accurately and not get-off one expected fields blank. When your application for the loan is actually inaccurate otherwise unfinished, it could impede brand new acceptance techniques. Definitely is most of the asked advice to get rid of delays.

This new FHA loan preapproval techniques usually takes five in order to 10 team days. This time physique may differ depending on facts including the lender’s work, the fresh complexity of your borrower’s financial situation together with responsiveness off this new debtor within the providing the called for documents. In many cases, you can get preapproval an identical big date.

How exactly to Boost Possibility of Delivering an enthusiastic FHA Financing Preapproval

You can take steps to increase your chance away from FHA home loan acceptance, out of improving your credit history so you can communicating with your bank. Listed below are three key information.

1. Maintain A good Economic Activities

It is necessary to look after a steady financial predicament while awaiting preapproval. Dont build biggest financial transform such as obtaining multiple playing cards or taking out fully an unsecured loan to find the latest chairs. Although it will likely be easy to jump to come and start planning for the future domestic, taking up more loans or to make other economic situations make a difference to the preapproval within the application processes.

2municate Together with your Financial

You could stay-in lingering correspondence with your bank on the preapproval way to ensure you bring any extra requisite documentation effectively. You can even ask the fresh lender’s suggestions and you will search explanation so you’re able to comprehend the FHA application for the loan processes from the contacting the loan officer. Exhibiting your engaged in the mortgage acceptance processes and you can ready to provide any requested documents punctually can increase the probability of acceptance.

step three. Be ready to Render A lot more Files

Even more documents may be required when you look at the finally underwriting process. To stop waits, has duplicates out of bank statements, spend stubs, tax statements and you may proof of almost every other offers such retirement profile so you’re able to reveal lenders when requested. It is very important getting quick and planned when getting such records to evolve recognition chance and reduce delays.

What is the Difference between FHA Financing Preapproval and you may Prequalification?

Throughout prequalification for an enthusiastic FHA mortgage, your earnings, property and you may borrowing from the bank is actually analyzed, and also you found a price off what you could qualify for. With preapproval, possible was explain to you the new automatic underwriting system to possess correct acceptance. While both are similar, prequalification ‘s the starting point to begin with determining your home to order energy.